For schools, houses of worship, museums, and similar institutions, accurate and timely reporting is not optional — it is a legal obligation tied directly to funding eligibility, audit exposure, and the ability to receive future awards.

Most non-profits only discover the operational complexity of federal grant reporting after receiving their first award. By then, deadlines are already running, submission systems need access requests, and regulatory obligations under 2 CFR Part 200 have already attached to the award. This guide walks through what reporting requires, how the process works, and where organizations most often get tripped up.

Key Takeaways

- Federal grant reporting is a mandatory post-award obligation — missed submissions can restrict or eliminate future funding

- Submit both financial reports (SF-425/FFR) and performance/progress reports, each with separate deadlines and systems

- FFATA requires transparency reporting through SAM.gov for subawards of $30,000 or more; FSRS.gov was retired in March 2025

- Missed deadlines, misaligned financials, and incomplete narratives are the three fastest ways to trigger a compliance finding

What Is Federal Grant Reporting?

Federal grant reporting is the structured, ongoing process through which grant recipients provide financial and programmatic accountability to the awarding federal agency. Reporting is entirely distinct from the application process — it begins the moment an award is made and continues until final closeout.

The process serves three concrete purposes:

- Public accountability — ensures taxpayer dollars are spent as authorized

- Program measurement — gives agencies the data needed to evaluate whether funded activities are achieving intended outcomes

- Continuation decisions — provides funders with the documentation required to approve renewal or follow-on awards

Understanding what sets federal reporting apart from other grant types helps non-profits calibrate their compliance approach from day one.

How Federal Reporting Differs from Private Grant Reporting

Federal grant reporting is far more tightly regulated than private or state grant reporting. Private funders typically set their own formats, timelines, and submission methods — flexibility is common.

Federal reporting operates differently. It is governed by specific statutes and regulatory frameworks — primarily the Federal Funding Accountability and Transparency Act (FFATA) and 2 CFR Part 200 (the Uniform Guidance) — and requires standardized forms submitted through designated federal systems.

OMB's 2024 final guidance for federal financial assistance, effective October 1, 2024, updated key thresholds and requirements that apply to all current awards.

Types of Federal Grant Reports Non-Profits Must Submit

Federal Financial Report (SF-425 / FFR)

The SF-425, also called the Federal Financial Report (FFR), is the primary financial reporting form. It tracks:

- Federal cash disbursements and expenditures

- Unliquidated obligations

- Unobligated balance of federal funds

- Recipient cost-sharing contributions (where applicable)

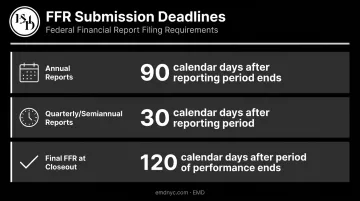

Deadlines under 2 CFR 200.328:

- Annual reports: due no later than 90 calendar days after the reporting period ends

- Quarterly/semiannual reports: due no later than 30 calendar days after the reporting period

- Final FFR at closeout: due no later than 120 calendar days after the period of performance ends

Most HHS-related awards submit FFRs through the Payment Management System (PMS). Access to PMS requires advance user registration, so set up your account well before your first deadline.

Performance and Progress Reports

These reports are the qualitative complement to the FFR — documenting what your organization actually did with the funding, not just how it was spent.

Required content includes:

- Activities conducted during the reporting period

- Milestones reached and populations served

- Outcomes achieved against stated objectives

- Deviations from the original project plan

- Challenges encountered and corrective actions taken

Submission systems vary by agency. DOJ recipients submit through JustGrants. NIH recipients submit Research Performance Progress Reports (RPPRs) through eRA Commons. FEMA recipients — including NSGP awardees — use FEMA GO. Each program's Notice of Award specifies the applicable system and schedule.

FFATA Subaward Reporting

Non-profits acting as prime awardees that pass federal funds to sub-recipients must report those arrangements under FFATA, implemented through 2 CFR Part 170.

Key requirements:

- Report any first-tier subaward that equals or exceeds $30,000 in federal funds

- Report modifications that bring a subaward to or above the $30,000 threshold

- FSRS.gov was retired on March 8, 2025 — all subaward reporting now occurs through SAM.gov

- Executive compensation reporting applies when an entity received 80% or more of annual gross revenues from federal awards and $25,000,000 or more in such revenues in the preceding fiscal year

Single Audit Requirement

Under 2 CFR 200.501, non-profits that expend $1,000,000 or more in federal awards during a fiscal year must undergo an independent Single Audit. This threshold increased from $750,000 to $1,000,000 under OMB's 2024 guidance, effective October 1, 2024.

The audit results — including the SF-SAC data collection form and reporting package — must be submitted to the Federal Audit Clearinghouse (FAC) at fac.gov within 30 calendar days of receiving the auditor's report, or nine months after the end of the audit period, whichever comes first. Organizations below the $1,000,000 threshold are exempt, though they must still retain records available for federal review.

SAM.gov Responsibility/Qualification Reporting

Non-profits with cumulative active federal awards exceeding $10,000,000 must maintain current integrity and performance data in SAM.gov's responsibility/qualification records and update them at least semiannually throughout the award period.

How the Federal Grant Reporting Process Works

The reporting cycle begins the moment the Notice of Award (NoA) is issued and runs continuously through each budget period until final closeout. The NoA is the governing document: it specifies exact reporting schedules, required formats, submission systems, and any award-specific conditions beyond standard 2 CFR 200 requirements. Read it on day one and keep it accessible for the life of the award.

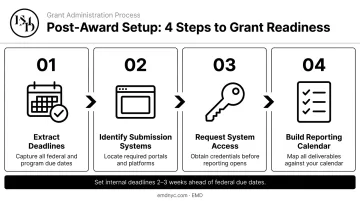

Step 1: Review the Notice of Award and Build a Reporting Calendar

Immediately after receiving the NoA:

- Extract every reporting deadline — financial reports, performance reports, and any special conditions

- Identify the submission systems required for each report type

- Request user access for PMS, SAM.gov, and any agency-specific portals before you need them

- Build a reporting calendar with internal preparation deadlines set at least two to three weeks ahead of federal due dates

The contacts listed in the NoA (which may include a Program Officer, Grants Management Officer, or Grants Management Specialist depending on the agency ) are your primary points of escalation when questions arise.

With your calendar built and contacts identified, the next priority is keeping the data clean throughout the award period.

Step 2: Track Financial and Programmatic Data Continuously

Effective reporting depends on documentation collected throughout the award period, not assembled at deadline. During the award:

- Reconcile actual expenditures against approved budget categories in real time

- Document program activities and outputs as they occur

- Maintain organized records — invoices, contracts, attendance logs, outcome data — that substantiate both financial and performance reports

- Flag budget variances or project changes as they arise, rather than trying to explain them after the fact

Consistent documentation through Step 2 makes the financial reporting in Step 3 straightforward rather than a scramble.

Step 3: Prepare and Submit the SF-425 (FFR)

When preparing the FFR:

- Reconcile cash disbursements against approved budget categories

- Verify figures align with your organization's accounting records

- Confirm both Preparer and Certifier roles are active in PMS before the deadline

- Account for any cost-sharing or match requirements reflected in the report

The FFR and your accounting records must tell the same story. Discrepancies between the two are the first thing a program officer or auditor will flag.

Step 4: Prepare and Submit the Performance Report

A well-structured performance report answers four questions for agency reviewers:

- Activities and reach: What you did, what outputs were delivered, and which populations were served

- Outcomes: What changed as a result, measured against your stated objectives

- Deviations: What shifted from the original project plan and why it happened

- Projections: What you expect to accomplish in the upcoming period

Federal agencies expect transparency. A report that omits obstacles, delays, or scope changes signals poor stewardship. Reviewers know projects rarely run perfectly; what they're evaluating is your organization's awareness and responsiveness.

Key Factors That Affect Reporting Compliance

Internal Organizational Risk Factors

Several internal conditions directly influence whether an organization meets its reporting obligations:

- Losing a grants manager mid-award is one of the highest-risk scenarios for smaller nonprofits — coverage plans and documented procedures reduce that exposure

- Fund accounting that cleanly separates grant expenditures makes FFR preparation straightforward; commingled accounts create reconciliation headaches

- Skipping an internal review step before submission is a reliable way to introduce preventable errors — organizations that formalize this step catch most problems before they reach the agency

Award Complexity and Reporting Burden

Not all federal awards carry equal reporting obligations. These factors add layers of obligation:

- Multi-year awards with multiple budget periods and separate FFR deadlines per period

- Awards with cost-sharing or match requirements that must be tracked and reported separately

- Grants with subaward structures that trigger FFATA reporting obligations

- Awards from agencies with specialized systems — FEMA GO for NSGP recipients, JustGrants for DOJ, eRA Commons for NIH

NSGP awards from FEMA illustrate this clearly. The FY 2025 NSGP has a 36-month period of performance (projected September 2025 through August 2028) with quarterly financial reports and semiannual performance reports — plus mandatory EHP review for any physical modification to a facility.

For K-12 schools, museums, and houses of worship navigating these layered requirements, having dedicated post-award support can make the difference between clean compliance and missed deadlines. EMD provides post-award grant management specifically for programs like NSGP, covering EHP submission, procurement, drawdown, and closeout.

Common Mistakes Non-Profits Make in Federal Grant Reporting

Missing or Late Submissions

Late reports carry real consequences. Under 2 CFR 200.339, federal agencies may temporarily withhold cash payments, disallow costs, suspend the award, or withhold further federal funds when recipients fail to comply. NIH specifies that failure to submit complete, accurate, timely reports may result in closer monitoring, award delays, or conversion to reimbursement payment.

Extensions are available under 2 CFR 200.344 when justified — but they must be requested before the deadline, not after.

Misalignment Between Financial and Performance Data

A common audit flag: the FFR shows significant unspent funds while the performance report claims full activity completion — or vice versa. The two reports draw from the same award and must reconcile. Reviewers and auditors read them together, and inconsistencies raise questions about accuracy and stewardship.

Omitting Challenges, Changes, or Negative Outcomes

Federal agencies expect honest reporting, not perfect outcomes. Progress reports that omit project delays, scope changes, or underperformance are technically incomplete — and they undermine credibility when the financial data tells a different story. Document what happened, note the reason, and describe the corrective steps your organization has taken.

Confusing Requirements Across Multiple Awards

Non-profits managing several federal grants simultaneously sometimes apply one award's reporting schedule or format to another. There is no universal federal reporting template. Each award's NoA governs its own requirements, and mixing requirements across awards produces submissions that are incomplete, noncompliant, or both. Treat each award's NoA as the governing document — not a general reference.

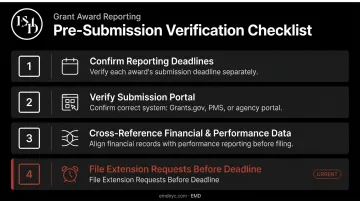

A quick checklist helps here:

- Confirm each award's reporting deadlines separately

- Verify the correct submission portal (Grants.gov, Payment Management System, agency-specific system)

- Cross-reference financial and performance data before submitting

- File extension requests before — never after — the deadline

Conclusion

Federal grant reporting is a sustained compliance obligation. It starts with the Notice of Award, runs through every budget period, and does not end until final reports are accepted at closeout.

Meeting that obligation means maintaining accurate financial tracking, submitting honest performance documentation, and hitting deadlines across multiple systems and report types — consistently, for the full period of performance.

For non-profits in security-critical sectors — K-12 schools, museums, transit authorities, houses of worship — managing these obligations correctly protects both current funding and future award eligibility. EMD supports organizations through every phase of this process — from security grant application and EHP submission to procurement, drawdown, and closeout — so nothing falls through the cracks when it matters most.

Frequently Asked Questions

What are federal grant reporting requirements?

Federal grant reporting requirements are the post-award obligations set out in each grant's Notice of Award. They typically include an annual Federal Financial Report (SF-425), a performance or progress report, and FFATA transparency disclosures — with specific deadlines, formats, and submission systems that vary by awarding agency.

What is an SF-425 (Federal Financial Report)?

The SF-425 (Federal Financial Report) is the standardized form grant recipients use to report how award funds were spent during a budget period. For most HHS-related awards, it is submitted through the Payment Management System (PMS) and is due within 90 days after each reporting period closes.

Who needs to file FFR (SF-425) reports?

Any organization that receives a direct federal grant award must file the SF-425 for each budget period. Exceptions exist — NIH's Streamlined Noncompeting Award Process (SNAP), for instance, applies a different schedule to eligible NIH awards — so always check your Notice of Award.

Is FFATA reporting still required?

Yes. FFATA reporting remains required. FSRS.gov was retired on March 8, 2025, and all subaward reporting now occurs through SAM.gov. Prime awardees must disclose first-tier subawards of $30,000 or more and, where applicable, executive compensation information.

What happens if a non-profit misses a federal grant reporting deadline?

Under 2 CFR 200.339, agencies can withhold payments, disallow costs, or suspend the award — and NIH may convert to reimbursement-only payment. Beyond immediate penalties, late reports delay fund access and can weaken your standing for future awards.

What is the difference between a financial report and a performance report for federal grants?

The SF-425 accounts for how grant funds were spent against the approved budget. The performance or progress report documents what activities were conducted, what outcomes were achieved, and how the project is tracking against its stated objectives. Both are required, and the numbers in each report must reconcile with each other.