Introduction

Federal grants fund some of the most important safety infrastructure in the country — security upgrades for K-12 schools, hardening projects for houses of worship, surveillance systems for transit authorities, and access control for museums. Programs like FEMA's Nonprofit Security Grant Program (NSGP), which had $274.5 million available in FY2025, and the COPS School Violence Prevention Program (SVPP), offering up to $500,000 per award, represent real opportunities for organizations to protect the people they serve.

Federal funding comes with obligations. Recipients must navigate regulations, reporting deadlines, procurement rules, and documentation requirements — and a single misstep can trigger clawbacks, audits, or full award termination.

This guide breaks down the key regulatory frameworks, core compliance requirements, and actionable best practices every recipient needs to manage a federal security grant without putting the award at risk.

Key Takeaways

- Federal grant compliance spans financial management, procurement, reporting, and record retention — from award issuance through close-out

- The primary regulatory framework is 2 CFR Part 200 (Uniform Guidance), updated in 2024 with key changes including a raised single audit threshold

- Non-compliance can result in fund clawbacks, audit findings, debarment, and loss of future award eligibility

- Single audits are now required when an entity expends $1 million or more in federal funds in a fiscal year (for fiscal years beginning on or after October 1, 2024)

- Organizations using NSGP or SVPP funding should treat procurement, EHP submission, and documentation as high-risk compliance areas at award

What Federal Grant Compliance Is and Why It Matters

Federal grant compliance is the ongoing process of meeting every regulatory, financial, and programmatic obligation attached to a federal award — not just at year-end, but continuously from the moment funds are received through final close-out.

Under 2 CFR 200.303, recipients must establish, document, and maintain effective internal controls that provide reasonable assurance of compliance with federal statutes, regulations, and award terms. Compliance isn't a year-end filing exercise — it's a control system woven into how the organization operates day to day, covering every obligation from procurement to final close-out.

The Four Pillars

Every recipient must uphold four core obligations:

- Adherence to grantor regulations — following applicable federal statutes, agency guidance, and grant-specific conditions

- Timely reporting — submitting financial and performance reports on schedule

- Accurate financial record-keeping — maintaining separate, documented accounting for each award

- Restricted fund use — spending only on approved, budgeted purposes

Consequences of Getting It Wrong

The stakes are significant. Under 2 CFR 200.339, remedies for non-compliance include:

- Temporary withholding of payments or reimbursements

- Disallowance and clawback of questioned costs

- Suspension or termination of the award

- Suspension or debarment from future federal awards

- Referral for legal action in cases of intentional misuse

Real-world audits confirm these aren't theoretical risks. A June 2025 DOJ OIG audit of a $500,000 SVPP grant to a school district found late single audits, incomplete property records for 11 of 21 tested items, a local match shortfall, and missed quarterly financial reports — all from a single award.

For organizations in security-sensitive sectors — K-12 schools, houses of worship, transit systems, cultural institutions — these failures carry especially high stakes. The funded projects exist to protect people, and non-compliance doesn't just jeopardize reimbursement; it can halt construction, delay security upgrades, and damage the organization's standing with the agencies it depends on for future funding.

That's the practical reality behind post-award grant management. EMD's structured 12-to-18-month engagement covers procurement, EHP submission, progress reporting, drawdown management, and close-out — addressing roughly 80% of the compliance workload that tripped up the organizations in audits like the one above.

The Regulatory Framework Governing Federal Grants

Federal grant compliance operates under a layered hierarchy — and every level applies at the same time.

The Hierarchy

From top to bottom:

- Authorizing legislation — the statute that created the grant program

- 2 CFR Part 200 (Uniform Guidance) — the primary administrative, cost, and audit standards framework

- Agency-specific guidance — FEMA's Preparedness Grants Manual, COPS Office Award Owner's Manuals, and program-specific notices of funding opportunity

- The Notice of Award — recipient-specific conditions layered on top of everything else

Each level must be read together. Agency conditions can be more restrictive than Uniform Guidance, and the Notice of Award often adds requirements that aren't obvious from the CFR alone.

2 CFR Part 200 and the 2024 Updates

The Uniform Guidance is the backbone of federal grant administration. It covers uniform administrative requirements, cost principles, procurement standards, and audit requirements for virtually all federal award recipients.

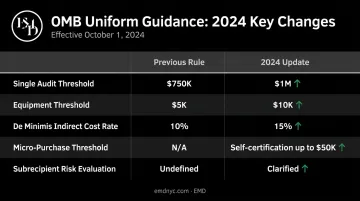

OMB's 2024 final rule, published April 22, 2024 and effective October 1, 2024, introduced several important changes:

- Single audit threshold increased from $750,000 to $1,000,000

- Equipment threshold increased from $5,000 to $10,000

- De minimis indirect cost rate increased from 10% to 15% of modified total direct costs

- Micro-purchase threshold self-certification option up to $50,000 under specified conditions

- Subrecipient risk evaluation requirements clarified for pass-through entities

The Single Audit

Entities that expend $1,000,000 or more in federal funds during a fiscal year must undergo a single audit — a combined financial and compliance review assessing whether funds were used appropriately. The $750,000 threshold applies only to fiscal years beginning before October 1, 2024.

Transparency Laws

The audit framework sits alongside two federal transparency statutes that extend accountability beyond the audit itself:

- FFATA (Public Law 109-282) requires disclosure of entities receiving federal funds on a publicly searchable website

- DATA Act (Public Law 113-101) expands financial data standards across federal agencies

The Notice of Award

The grant agreement itself may impose conditions beyond 2 CFR Part 200: additional reporting frequency, Build America Buy America procurement requirements, pre-approval requirements for budget modifications, or environmental review obligations. Review it before obligating any funds.

For NSGP and SVPP recipients in particular, requirements can vary significantly by state even within the same federal program. EMD navigates this complexity as part of its post-award administration service, coordinating paperwork and processes with grant representatives on the client's behalf.

Core Compliance Areas Every Recipient Must Manage

Financial Management and Cost Allowability

Recipients must maintain a dedicated accounting system that tracks expenditures by grant, budget category, and project component. No co-mingling across awards. No charging costs to a grant because the budget has room — costs must be allocable to the activity being funded.

Under 2 CFR 200.403, allowable costs must be:

- Necessary and reasonable for the award purpose

- Properly allocated to the funded activity

- Consistently treated across the organization

- Adequately documented

- Not used to satisfy cost-sharing on another federal award

Before making significant budget modifications, get prior written approval from the program office. Undocumented budget shifts are a common source of questioned costs during audits.

Procurement Standards

Federal procurement rules require open, competitive purchasing processes. 2 CFR 200.318 mandates written procurement procedures, documented procurement history, and written standards of conduct covering conflicts of interest. Anyone with a financial interest in a contract cannot participate in selecting, awarding, or administering it.

Procurement violations consistently appear among the most common single audit findings. For security equipment and installation contracts (the core deliverable of NSGP and SVPP awards) this means:

- Documented competitive solicitations (RFPs, bids, quotes depending on dollar threshold)

- Written selection rationales

- Conflict-of-interest certifications for all decision-makers

- Good-faith efforts to include disadvantaged business enterprises

The paper trail needs to exist before questions arise — not assembled afterward when an auditor is already asking.

Performance and Financial Reporting

Most federal awards require both financial reports (expenditures against the approved budget, submitted via SF-425) and programmatic reports (progress toward stated goals). Missing deadlines can delay reimbursements and trigger additional scrutiny from the awarding agency.

EMD manages progress reporting and drawdown management as core elements of its post-award engagement, ensuring clients stay current on submission schedules throughout the award period.

Internal Controls and Subrecipient Monitoring

Strong internal controls are built on three foundations:

- Segregation of duties — no single person controls authorization, execution, and recordkeeping for the same transaction

- Documented approval workflows — written sign-off requirements for expenditures, procurement decisions, and budget modifications

- Regular risk assessments — periodic reviews of where compliance exposure exists across the award period

The GAO's Green Book (most recently updated May 15, 2025, GAO-25-107721) provides the standard framework, effective beginning FY2026 with early implementation permitted.

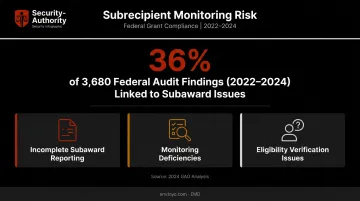

If a recipient passes federal funds to another organization (a subrecipient), the primary recipient remains responsible for that subrecipient's compliance. A 2024 GAO analysis of 3,680 audit findings from 2022–2024 found 36% were associated with incomplete subaward reporting, monitoring deficiencies, or eligibility verification issues — a persistent risk area that many recipients underestimate.

EHP Submission

For FEMA-funded physical security projects, Environmental and Historic Preservation (EHP) review is a mandatory pre-construction compliance step. No work can begin until EHP approval is secured. The process requires documentation of project scope, site conditions, and potential impacts. Approval typically takes 30 to 60 days depending on the state.

EMD manages EHP submission as a dedicated phase of its post-award administration, using the waiting period to finalize vendor alignment so clients can move immediately once approval comes through.

Best Practices for Building a Compliance-Ready Organization

1. Write your policies before you spend. Document budget management procedures, expense approval workflows, reporting schedules, and record retention rules before the first dollar goes out. Include grant managers, finance staff, and leadership in building these systems — they need to reflect how the organization actually operates, not an idealized process.

2. Train continuously, not once. Compliance requirements change. The 2024 Uniform Guidance updates are a clear example — teams that weren't tracking OMB's regulatory calendar were caught off guard. Designate a compliance lead for each active award with clear accountability, and subscribe to OMB and agency guidance updates as a routine practice.

3. Track by ALN from day one. Every federal award carries an Assistance Listing Number. Organizing expenditure records by ALN from the outset makes Schedule of Expenditures of Federal Awards (SEFA) preparation straightforward and demonstrates audit readiness throughout the award period.

4. Engage experienced external partners for complex programs. First-time NSGP or SVPP recipients often manage federal procurement rules, contractor oversight, EHP submissions, drawdown requests, and close-out reporting simultaneously — with no dedicated grants staff. A specialized grant administration firm like EMD handles that workload end-to-end, so school administrators, nonprofit directors, and facility managers can stay focused on their actual mission.

5. Reconcile monthly, not at year-end. Monthly reconciliation of grant expenditures against approved budgets catches problems while they're still correctable. By the time an annual audit surfaces a discrepancy, the remedy options are narrower.

Together, these five practices shift compliance from a reactive scramble to a built-in function — the difference between surviving an audit and never fearing one.

Audit Readiness and Record Retention

Maintaining Audit-Ready Files

Audit readiness is the result of consistent documentation habits — not a last-minute push before close-out. That means keeping the following current throughout the award period:

- Every expenditure tied to an approved budget line and backed by supporting documentation

- Procurement files complete from solicitation through contract execution

- Progress and financial reports filed on time and retained

- Property records current for any equipment purchased with grant funds

The June 2025 SVPP audit findings — incomplete property records, missed quarterly reports, a local match shortfall — are exactly the kind of problems that emerge when documentation is treated as a close-out task rather than an ongoing obligation. Knowing which records you're required to keep — and for how long — is the first step toward avoiding those gaps.

Records You Must Retain

Under 2 CFR 200.334, the following must be retained for at least three years from the date the final financial report is submitted (longer if an audit, claim, or litigation is pending):

- Notice of Award and approved grant application and budget

- All financial and programmatic reports

- Procurement files (RFPs, bids, conflict-of-interest certifications, selection rationales)

- Expenditure records (invoices, receipts, cancelled checks)

- Time and effort records for personnel charged to the award

- Equipment records (for items purchased with grant funds)

Proactive Audit Preparation

Three habits that make external audits far less stressful:

- Run quarterly internal reviews — spot-check compliance activities against a program-specific checklist each quarter

- Reconcile grant expenditures monthly — any discrepancy identified in month two is easier to address than one discovered in month fourteen

- Address internal findings immediately — document what went wrong, what corrective action was taken, and what process change prevents recurrence

EMD's grant administration work maintains organized, reviewer-ready files at every stage — from procurement through close-out — so clients have a complete, defensible record on hand if an auditor requests it.

Frequently Asked Questions

What does a grant compliance officer do?

A grant compliance officer oversees internal controls, monitors expenditures against approved budgets, coordinates audit activities, and keeps staff current on regulatory changes. In smaller organizations, this role is often assigned to a finance director or program manager as a secondary responsibility.

What is the difference between SF-270 and SF-425?

The SF-270 (Request for Advance or Reimbursement) is used to request payment from a federal agency. The SF-425 (Federal Financial Report) is a standardized form for reporting financial status and expenditures on an active award. One initiates payment; the other documents spending.

What is the Uniform Guidance (2 CFR Part 200)?

The Uniform Guidance is OMB's consolidated set of administrative requirements, cost principles, and audit standards that apply to most federal award recipients. It was most recently updated in 2024, with key changes including raising the single audit threshold to $1 million and increasing the equipment threshold to $10,000.

What happens if an organization fails a federal grant compliance audit?

Audit findings can result in:

- Repayment of disallowed costs

- Heightened oversight and additional reporting conditions

- Ineligibility for future federal awards

- Referral for legal penalties in cases of intentional misconduct

Findings also become part of the public record through the Federal Audit Clearinghouse.

What records are required to be retained for federal grants?

Recipients must retain all financial and programmatic records for at least three years after the grant is closed out. This includes the grant agreement, approved budget, expenditure documentation, procurement files, and submitted reports. Longer retention applies if an audit or legal matter remains open.

When is a Single Audit required?

A Single Audit is required when a non-federal entity expends $1,000,000 or more in federal funds during a fiscal year (for fiscal years beginning on or after October 1, 2024). It covers both financial statements and compliance with requirements that could have a direct and material effect on each major federal program.